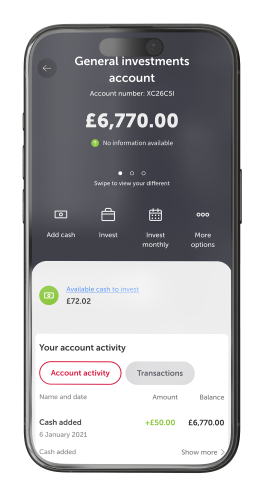

What is a general investment account?

A general investment account (GIA) is sometimes called a dealing account or trading account with other providers. Whatever you call it, it’s a flexible - but taxable - investment account. If you haven't used up your tax-free ISA allowance this year, you may want to look instead at the Dodl investment ISA.

For all the important details about the Dodl GIA, make sure you read its key features.

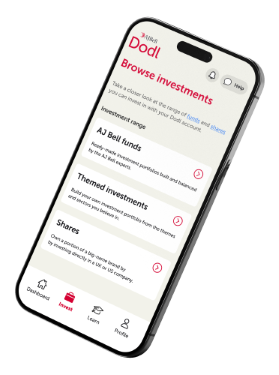

Why choose a Dodl general investment account?

Because Dodl keeps things simple. You can open your GIA and start your investing journey with as little as £25 a month. And here are just a few more reasons...

Investing is an opportunity to grow your money, typically outperforming cash savings over the long term. However, investing comes with risk as well as reward, and the value of your investments can go down as well as up. Tax benefits depend on your circumstances and tax rules may change. Any information we provide is to help with your research and isn't financial advice.

GIA charges

Like all Dodl accounts, you'll only pay one simple low-cost charge for your general investment account. Here's how it works.

How to get started

It’s as easy as 1-2-3 to get started with a Dodl GIA.

Like what you’re hearing? Download Dodl today to open your general investment account.